GM Hits the Brakes: $3.5 Billion Samsung SDI Battery Plant on Hold Amidst Cooling EV Demand

General Motors, once a vocal proponent of an aggressive all-electric future, has reportedly paused its ambitious $3.5 billion joint venture with Samsu...

Editorial Team

World Of EV

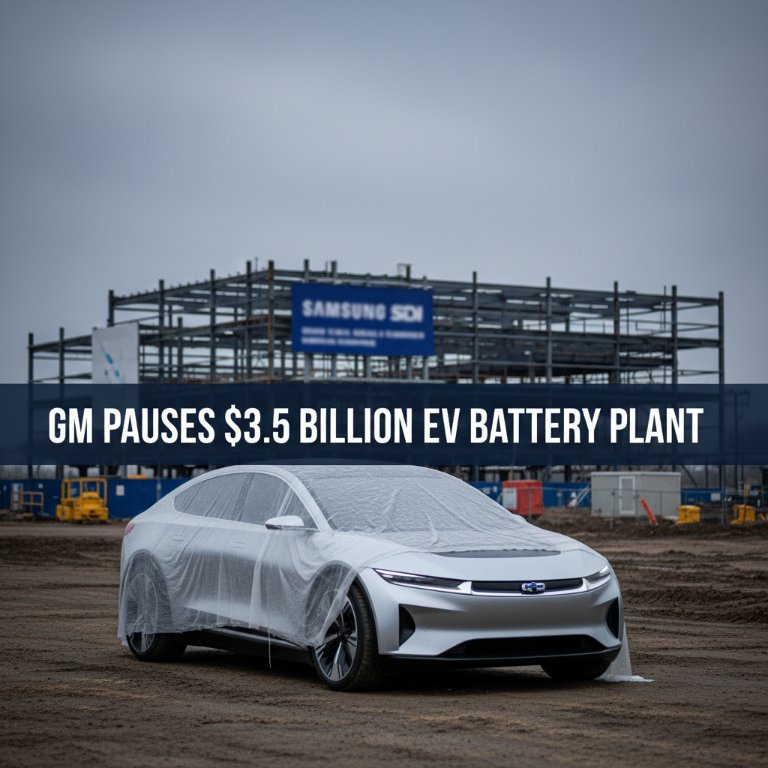

General Motors, once a vocal proponent of an aggressive all-electric future, has reportedly paused its ambitious $3.5 billion joint venture with Samsung SDI to construct a crucial EV battery manufacturing plant in Indiana. This significant development signals a clear recalibration of GM's electrification roadmap, directly influenced by what the automaker cites as lower-than-expected demand for electric vehicles in the U.S. and an ongoing reassessment of its overarching EV strategy.

The planned facility was a cornerstone of GM's strategy to secure its battery supply chain, with mass production initially slated for the fall of 2027. It aimed for an annual capacity of 36 GWh, enough to power approximately 300,000 electric vehicles annually, underpinning a substantial portion of GM's projected EV output for the coming years. The pause is more than a minor hiccup; it represents a substantial adjustment to its manufacturing timeline and commitment to specific battery chemistries, prompting widespread re-evaluation across the industry.

The Deal on Hold: A Jolt to GM's Ultium Ambitions

For years, General Motors has championed its Ultium battery and platform architecture as the bedrock of its electric revolution. The joint venture with Samsung SDI, announced with much fanfare, was intended to be GM's fourth battery plant in the U.S., supplementing its existing partnerships with LG Energy Solution. This expansion was critical for GM to achieve its lofty targets, including manufacturing 1 million EVs annually in North America by 2025. This latest pause casts a shadow over the feasibility of such aggressive timelines and the capital expenditure associated with them.

Shifting Tides: Lower Demand and Strategic Recalibration

GM's decision directly correlates with a broader industry trend: the tempering of EV sales growth. While still increasing, the rapid acceleration seen in prior years has begun to moderate, particularly in the U.S. market. Consumers are grappling with higher interest rates, ongoing concerns about charging infrastructure, and the persistent price premium of many new EVs. This has forced automakers, including GM, to reassess their production forecasts and investment strategies. The explicit mention of a “reassessment of its EV strategy” suggests that GM is not just tweaking production numbers but potentially rethinking its market segmentation, product rollout cadence, and even its approach to different battery technologies.

A Broader Trend? Battery Chemistry Considerations

The source material also hints at a “potential shift in preferred battery chemistries.” This is a critical point of expert analysis. Traditionally, GM, like many Western automakers, has focused heavily on nickel-cobalt-manganese (NCM) chemistries for their higher energy density and range. However, Chinese manufacturers, notably BYD with its Blade battery and Tesla, have increasingly embraced lithium iron phosphate (LFP) batteries for their lower cost, greater thermal stability, and longer cycle life, albeit with slightly lower energy density. If GM is indeed considering a stronger pivot to LFP, this pause could be an opportunity to re-evaluate the plant's design and equipment to better suit LFP production, or even to explore different supplier relationships more attuned to LFP technology. Such a shift would allow GM to offer more affordable EV models, a crucial factor in stimulating broader market adoption.

Why This Matters:

For GM's Electrification Timeline: The immediate impact is a likely delay in GM's ability to scale its EV production. While it has existing battery ventures, the Indiana plant was key to meeting its aggressive internal targets. This pause could push back the availability of certain EV models or slow the pace of price reductions that depend on localized, high-volume battery production.

For Samsung SDI: This represents a significant setback for Samsung SDI's expansion plans in North America, a crucial market for battery manufacturers. While the partnership might eventually proceed, the delay means lost revenue and potentially a reshuffling of its global investment strategy.

For the U.S. EV Market: This signals a growing caution among major automakers regarding the pace of EV adoption. It could lead other manufacturers to re-evaluate their own large-scale investment plans, potentially slowing the overall transition to electric vehicles in the U.S. Consumers might interpret this as a sign of uncertainty, reinforcing hesitant buying decisions.

For Battery Technology Evolution: The hint at a shift in preferred battery chemistries suggests that the industry is rapidly adapting to market demands for more affordable EVs. This could accelerate the adoption of LFP batteries in mainstream models, putting pressure on battery suppliers to diversify their offerings and on automakers to integrate these new technologies efficiently. Who wins? Automakers agile enough to adapt their battery strategies and suppliers with diverse chemistry portfolios. Who loses? Companies overly committed to a single chemistry or a rigid production timeline.

The Road Ahead: A Prudent Pause or a Stumbling Block?

General Motors' decision to halt its $3.5 billion battery plant with Samsung SDI is a stark indicator of the evolving and often unpredictable nature of the electric vehicle market. While framed as a strategic reassessment, it highlights the challenges automakers face in balancing ambitious electrification goals with real-world market demand and economic pressures. The coming months will reveal whether this pause is a prudent recalibration allowing GM to emerge stronger with a more resilient and cost-effective EV strategy, or if it represents a significant stumbling block on its path to an all-electric future. The automotive world, and particularly the EV community, will be watching closely to see how this influential automaker navigates these turbulent waters.